W O R K I N G P A P E R S

Interest Rate Surprises When the Fed Doesn’t Speak

Silvia Miranda-Agrippino and John C. Williams (2026), CEPR Discussion Paper No. 21056

✏️ January 2026

ABSTRACT The predictability of monetary policy surprises based on past, public information has been interpreted in two related yet fundamentally different ways. The “Fed information effect” posits that it arises due to markets updating their view of the economy, based on signals implicitly revealed by the FOMC. The “Fed reaction to news” explanation posits that markets update their view of the FOMC's reaction function instead. We show that interest rate surprises calculated around macroeconomic releases exhibit the same predictability pattern as monetary policy surprises, at a time when there is no scope for markets to learn about the Fed's behaviour.

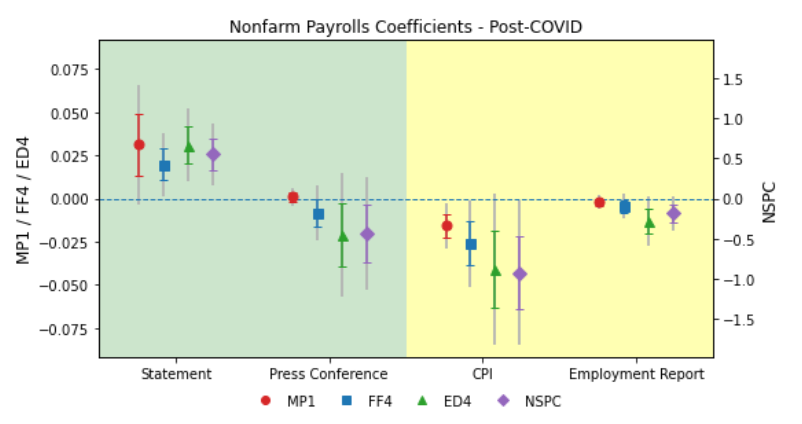

Financial Market Effects of FOMC Communication: Evidence from a New Event-Study Database

Miguel Acosta, Andrea Ajello, Michael Bauer, Francesca Loria and Silvia Miranda-Agrippino, FRBSF WP 2025-30 (2025)

✏️ December 2025

💾 USMPD

ABSTRACT This paper introduces the U.S. Monetary Policy Event-Study Database (USMPD), a novel, public, and regularly updated dataset of financial market data around Federal Open Market Committee (FOMC) policy announcements, press conferences, and minutes releases. Using the rich high-frequency data in the USMPD, we document several new empirical findings. Large monetary policy surprises have made a comeback in recent years, and post-meeting press conferences have become the most important source of policy news. Monetary policy surprises have pronounced negative effects on breakeven inflation based on Treasury yields. Risk assets, including dividend derivatives, also respond strongly and negatively to monetary policy surprises, consistent with conventional channels of monetary transmission. Press conferences have stronger effects than FOMC statements on most asset prices. Finally, the term structure evidence shows peak effects on market-based inflation and dividend expectations at horizons of several years.

The Ins & Outs of Chinese Monetary Policy Transmission

Silvia Miranda-Agrippino, Tsvetelina Nenova and Hélène Rey (2025), CEPR Discussion Paper No. 20958

✏️ December 2025

MEDIA 📰 Mapping the Contours of Chinese Policy Transmission (VoxEU, VoxChina)

ABSTRACT We estimate a policy rule for the People’s Bank of China that accounts for the dual nature of its price stability mandate—encompassing domestic inflation and the exchange rate—and for the evolution of its operational framework. A single novel policy indicator summarises the multidimensional monetary policy that relies on multiple tools with different intensities over time. The Ins: The domestic transmission of Chinese monetary policy follows textbook patterns, with exceptions due to the active management of the renminbi and of the financial account. The Outs: Internationally, fluctuations in Chinese monetary policy affect primarily commodity markets, and with them global production and trade. The pass-through of commodity price changes to foreign (US) producer and consumer prices is substantial. Financial spillovers are second-order, and mostly derivative from trade spillovers.

Global Footprints of Monetary Policies 💾

Silvia Miranda-Agrippino, Tsvetelina Nenova and Hélène Rey (2020), Centre for Macroeconomics, Discussion Paper n. 2020-04

✏️ First Draft January 2020

ABSTRACT We study the international transmission of the monetary policy of the two world’s giants: China and the US. From East to West, the channels of global transmission differ markedly. US monetary policy shocks affect the global economy primarily through their effects on integrated financial markets, global asset prices, and capital flows. EMEs in particular see both a reduction in inflows and a surge in outflows when the market tide turns as a result of a US monetary contraction. Conversely, international trade, commodity prices and global value chains are the main channels through which Chinese monetary policy transmits worldwide. AEs with a strong manufacturing sector are particularly sensitive to these disturbances.

Unsurprising Shocks: Information, Premia, and the Monetary Transmission 💾

Silvia Miranda-Agrippino (2016) Bank of England, Working Paper n. 626

✏️ Revised August 2017

MEDIA 📰 The surprise in monetary surprises: a Tale of Two Shocks (Bank Underground Blog) 📰 Wall Street Journal Pro Central Banking

ABSTRACT This article studies the information content of monetary surprises, i.e. the reactions of financial markets to monetary policy announcements. We find that monetary surprises are predictable by past information, and can incorporate anticipatory effects. Surprises are decomposed into monetary policy shocks, forecast updates, and time-varying risk premia, all of which can change following the announcements. Hence, their use as identification devices is not warranted, and can have strong qualitative and quantitative implications for the estimated responses of variables to the shocks. We develop new measures for monetary policy shocks, independent of central banks’ forecasts and unpredictable by past information.

Nowcasting China

Domenico Giannone, Silvia Miranda-Agrippino and Michele Modugno, 2013

MEDIA 🎥 Interview at CIRANO Montréal

ABSTRACT In this paper we construct a synthetic indicator to monitor and summarise the informational content of the Chinese macroeconomic data flow. The index is optimally extracted in real-time from a heterogeneous set of dat, published at different frequencies and in a non-synchronous fashion, that we select to best represent the Chinese economy. We evaluate the forecasting ability of the index in nowcasting Chinese real GDP in real time. We find that the forecast implied by our index are at least as accurate as market forecasts and outperform forecasts implied by other existing indices. Furthermore, our index-based forecasts are continuously updated and thus timelier than forecasts implied by other existing indices or produced by international institutions, including the IMF and the OECD.